Weekly housing inventory data

While inventory growth this week slowed to 6,803 — well below my weekly target level of 11,000 -17,000 with elevated mortgage rates — the fact that we hit this target level five times this year versus zero last year is a big reason why 2024 has been a much better year for housing than 2023. As we can see below, it’s a much healthier year in inventory growth data than in 2023.

- Weekly inventory change (June 29-July 5): Inventory rose from 645,770 to 652,573

- The same week last year (June 30-July 7), Inventory rose from 466,534 to 466,001

- The all-time inventory bottom was in 2022 at 240,497

- This week is the inventory peak for 2024 at 652,573

- For some context, active listings for this week in 2015 were 1,183,882

New listings data

We are at the seasonal peak period for new listings. We will soon be getting into the weekly decline period of this data line, and while we have showed growth year over year, we never got to my minimum target level of 80,000. Here are the new listings for last week over the past few years:

- 2024 71,181

- 2023: 58,289

- 2022: 89,221

Price-cut percentage

In an average year, one-third of all homes take a price cut — this is standard housing activity. As rates have stayed elevated, the price-cut percentage is higher than in the last two years, and certain pockets of the U.S. have higher inventory data than the national data.

A few weeks ago, on the HousingWire Daily podcast, I discussed that the price-growth data will cool down in the second half of the year.

Here are the price-cut percentages for last week over the previous few years:

- 2024: 38%

- 2023: 33%

- 2022: 32%

Pending sales

Below is the Altos Research weekly pending contract data year-over-year to show real-time demand. With more sellers who are buyers, we have a tad more demand this year. This week showed very little year-over-year growth and there is also a holiday week effect here. For the entire year, we have shown a tiny bit of growth in the pending contracts; this data line can grow year over year when mortgage rates fall, but we haven’t had that happen so far in 2024 in any meaningful way with duration.

So far, our pending contract data is still showing growth:

- 2024: 381,057

- 2023: 381,036

- 2022: 420,816

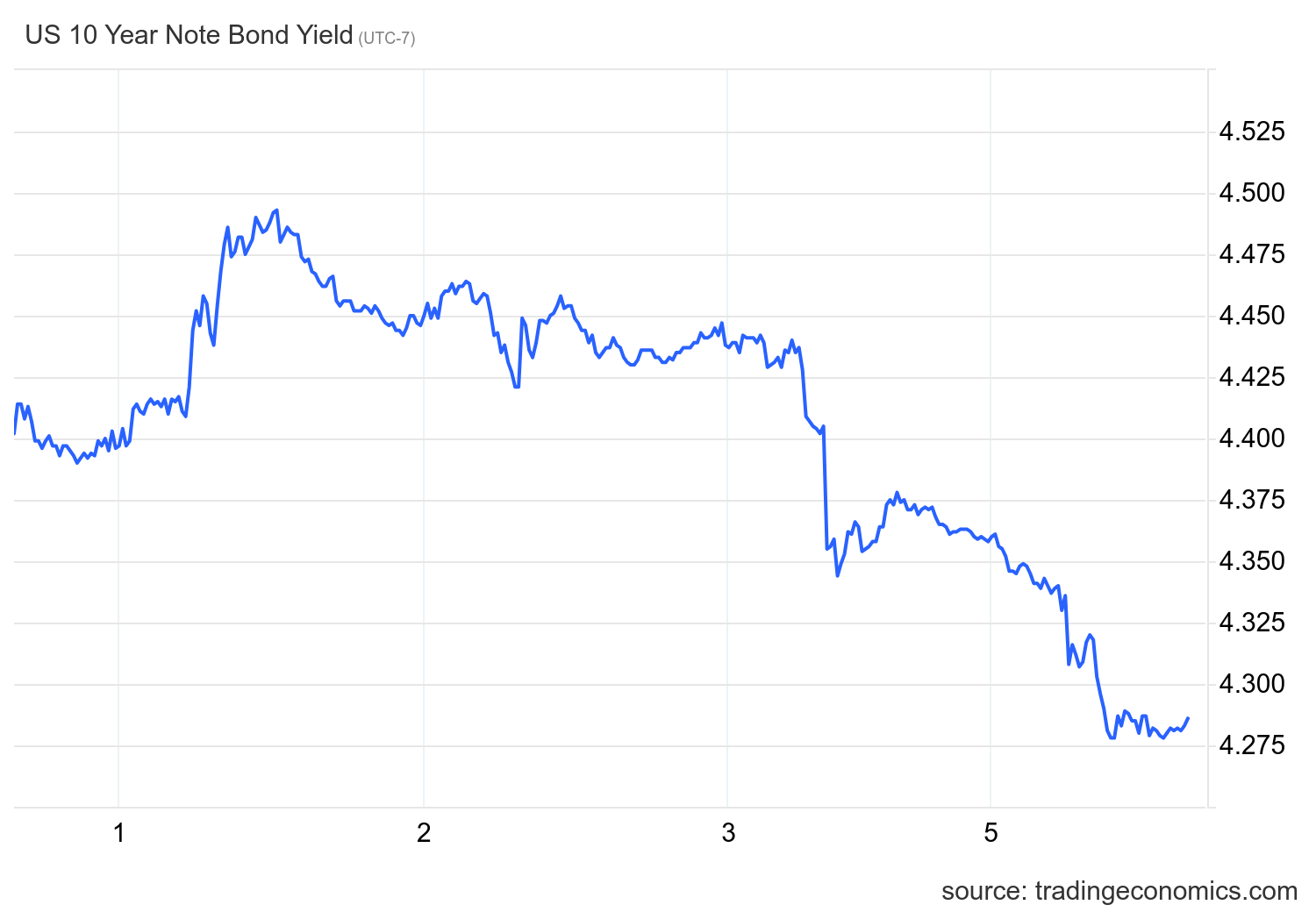

10-year yield and mortgage rates

Two weeks ago, the 10-year yield had a crazy move higher, even with softer inflation data. Last week, we returned close to recent lows. Here is how the 10-year yield acted with jobs week, which once again is showing the labor market getting softer but not breaking yet.

Then we had Jobs Friday, in which the headline number looked fine, but the internal labor reports lately look softer, which is what the Federal Reserve has wanted all along. I wrote about the recent jobs week data here.

After the jobs report, bond yields headed lower and trended lower the entire day on Friday, July 5, which you can see in the chart below — dragging mortgage rates lower with them.

Mortgage spreads

The spread between the 30-year mortgage rate and the 10-year yield has been an issue since 2022, and things got worse after the March 2023 banking crisis. However, this year, spreads have improved.

If we took the worst levels of the spreads from 2023 and incorporated those today, mortgage rates would be 0.56% higher right now. While we are far from being average with the spreads, the fact that we have seen this improvement is a plus this year.

Purchase application data

The three-week winning streak of purchase application data ended last week as rates had risen in the previous weeks. This shows once again how even weekly moves up and down can flip this data line from positive to negative.

Since the onset of falling mortgage rates in November 2023, we’ve seen 15 positive prints, 14 negative prints and two flat prints in the week-to-week data. However, as mortgage rates began to rise earlier this year, we observed a decline in demand. The year-to-date data for 2024 is unfavorable, with 9 positive prints, 14 negative prints and two flat prints. If mortgage rates can head lower and stay lower with duration, we can grow application data purely based on the fact that we are working from the lowest levels ever once adjusting to our workforce growth.

The week ahead: Inflation, Powell testimony, auctions and fed speeches

It’s inflation week again. We have CPI inflation and PPI inflation reports coming up on Thursday and Friday. Fed Chairman Jerome Powell will give testimony before Congress on Tuesday and we will also have more Fed presidents speaking next week. The key is to see if any recent labor data softness changes their tune.

We will also have a few bond auctions. It’s hard to break under 4.20% on the 10-year yield, so we shall see if this week that happens or if we still stay in the range between 4.20% and 4.50%.