Mortgage rates moved massively lower last week without any Federal Reserve rate cuts, primarily because the labor market is getting softer. Can mortgage rates go even lower?

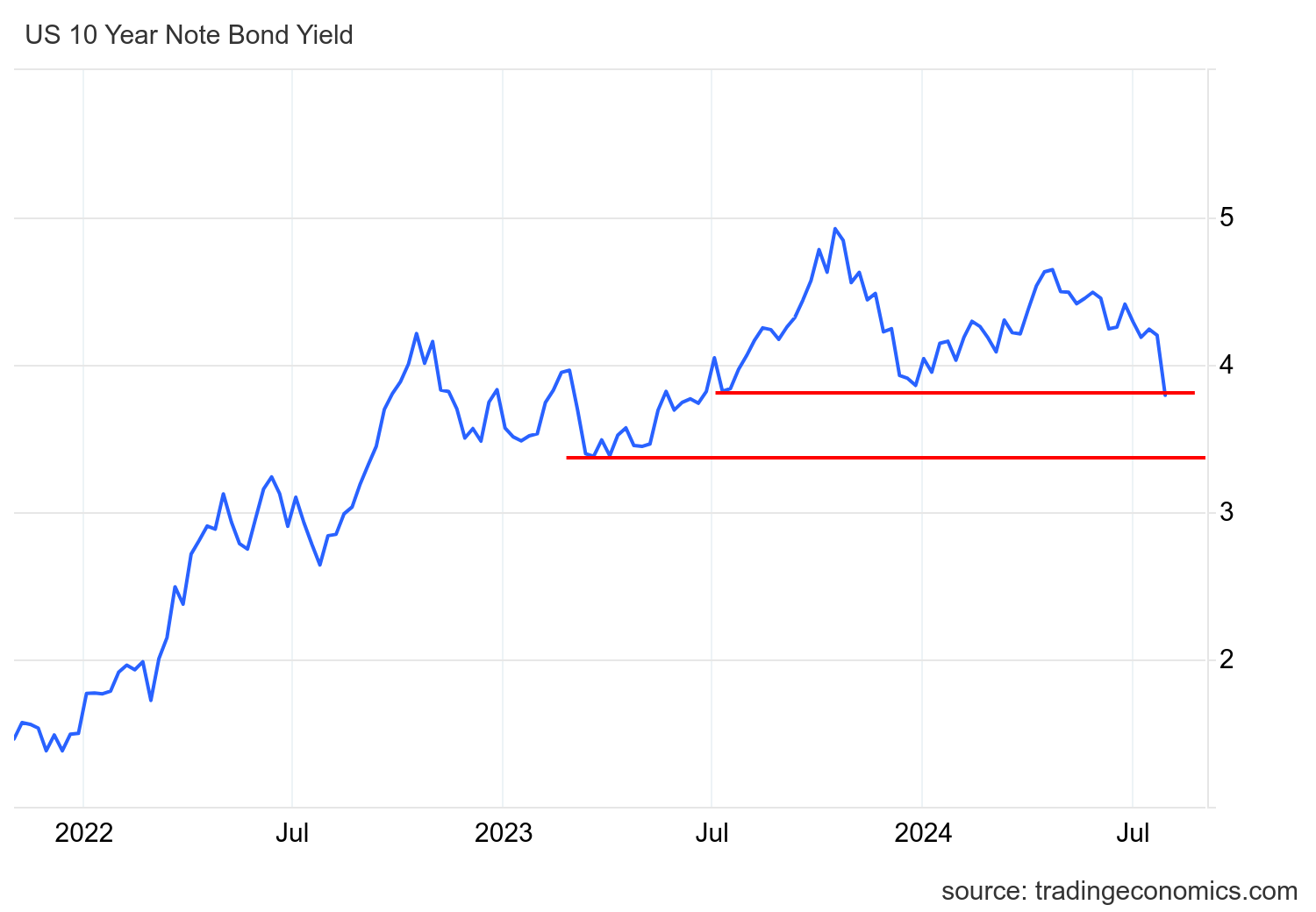

As we can see below, when the market priced economic weakness earlier in 2024, it took the 10-year yield down toward 3.80% but didn’t break that level. So, after a softer jobs report, the question is: Can this level break and head back down to the key line in the sand I call the Gandalf line at 3.37%? I wrote about Friday’s jobs report and discussed all the labor data we got last week here.

10-year yield and mortgage rates

My 2024 forecast included

- A range for mortgage rates between 7.25%-5.75%

- The 10-year yield between 4.25%-3.21%

The 10-year yield reached as high as 4.70% this year as economic data was beating estimates early on with hotter inflation data, but mortgage rates didn’t follow as closely as last year because the mortgage spreads have gotten better in 2024. However, the labor data has been getting softer for many months. So, now we are at a critical spot for the 10-year yield around the 3.80% level.

Since the Fed hasn’t pivoted or cut rates, it’s up to the bond market to do the heavy lifting for the Fed, who are behind the curve on purpose. To break noticeably from here, we need to continue to see softer data.

Mortgage spreads

Mortgage spreads were a negative storyline in 2023 as the Silicon Valley Bank collapse and the resulting banking crisis pushed the spreads to new cycle highs. We don’t have that variable this year and spreads have improved earlier than I thought, which has helped mortgage pricing. We have a lot of room to the downside on spreads, too.

If we took the worst levels of the spreads from 2023 and incorporated those today, mortgage rates would be 0.49% higher right now. While we are far from being average with the spreads, the fact that we have seen this improvement is a plus this year.

Purchase application data

Since mortgage rates have fallen recently, purchase application data has been flat, with four positive and four negative weeks. However, the three straight weeks of purchase application data growth we saw early in June filtered into the pending home sales data, which shocked everyone with a beat to the upside. Remember, we were working from the lowest levels in history so moving the needle doesn’t take much. This last week was another negative print.

Since mortgage rates started to fall in November 2023, we’ve seen 16 positive prints, 17 negative prints and two flat prints in the week-to-week data. However, as mortgage rates began to rise earlier this year, we observed a decline in demand. The year-to-date data for 2024 is still unfavorable, with 10 positive prints, 17 negative prints and two flat prints.

Weekly housing inventory data

The best story in 2024 has been inventory growth. We can’t have a functional housing market with the inventory levels we saw from 2020-2023. This year we’ve gotten enough inventory growth to create a buffer so we don’t have another savagely unhealthy housing market when mortgage rates fall. I talked about this on CNBC recently.

For 2024, my model is straightforward: with higher rates we should get weekly inventory growth between 11,000 and 17,000 homes. We have done this six times this year, something that didn’t happen even once last year. As rates have fallen In the last two weeks, we haven’t hit those levels, but there is good enough growth for me to keep smiling until the seasonal decline.

Last week inventory grew by 6,482. I stress that we needed this to have a regular housing market ever again!

- Weekly inventory change (July 26-Aug. 2): Inventory grew from 677,246 to 683,728

- The same week last year (July 27-Aug. 3): Inventory rose from 485,743 to 488,607

- The all-time inventory bottom was in 2022 at 240,497

- The yearly inventory peak for 2024 is this week at 683,728

- For some context, active listings for this week in 2015 were 1,195,876

New listings data

Another positive story has been the new listings data, a key variable on why inventory growth is happening this year. While I didn’t get my minimum target of 80,000 new listings during the peak seasonal weeks this year, it was good to see growth. The seasonal decline we see now is very normal.

Here are the number of new listings for last week over the previous several years:

- 2024: 67,085

- 2023: 60,766

- 2022: 73,177

Price-cut percentage

In an average year, one-third of all homes take a price cut — this is standard housing activity. As mortgage rates have stayed elevated, the price-cut percentage is higher than in the last two years and certain pockets of the U.S. have higher inventory than the national data. Remember that we are working from all-time lows in demand when adjusting to the labor force growth.

A few weeks ago, on the HousingWire Daily podcast, I discussed that the price-growth data will cool down in the year’s second half. Here are the price-cut percentages for last week over the previous few years:

- 2024: 39%

- 2023: 35%

- 2022: 38%

Pending sales

Below is the Altos Research weekly pending contract data year-over-year to show real-time demand. With more sellers who are buyers, we have a bit more demand this year. Purchase application data tends to look out 30-90 days, and the only time we saw any real growth in purchase apps was at the end of 2022 and 2023, when rates fell more than 1%.

- 2024: 379,482

- 2023: 364,934

- 2022: 405,466

The week ahead

It will be a calm week on the data front, but we will have an interesting Monday with the ISM and PMI reports, especially the service sector report. We have some bond auctions this week and Fed President Barkin will speak. All Fed presidents’ speeches will be looked at more closely now since the unemployment rate is at 4.3%.